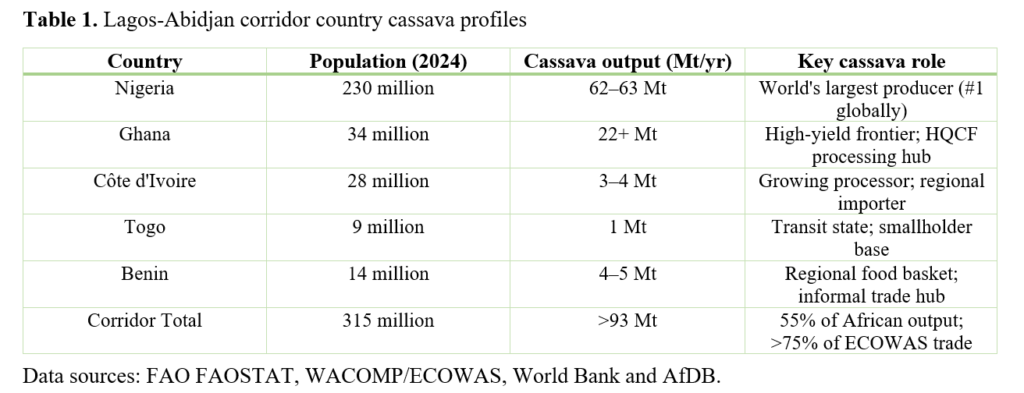

West Africa produces over 93 million tonnes of cassava annually, 55% of African output and a third of global production yet captures less than 1% of global cassava export value. Nowhere is this paradox more visible, or more solvable, than along the 1,028-kilometre coastal arc linking Lagos to Abidjan through Benin, Togo, and Ghana, a corridor home to 200 million people, accounting for over 75% of ECOWAS trade flows and a combined GDP exceeding $700 billion. At the recent AUDA-NEPAD/ECOWAS/ECDPM stakeholder meeting on cassava industrialisation along this corridor, where I had the opportunity to present an updated mapping of the digital tools already transforming the value chain, the conversation made clear that AKILIMO, PlantVillage Nuru, Cassava Seed Tracker, Cassava Business Connector, TropiConnect, FarmERP, and similar platforms are delivering measurable gains in productivity, traceability, and farmer income. Strengthening the productive base, however, is only half of the equation that the 1% paradox demands.

The convergence of three forces makes 2026 a watershed moment: (1) a $15.5 billion highway project breaking ground this year that will reduce transit times and logistics costs significantly; (2) ballooning global demand for cassava-derived industrial products including starch, glucose, bioethanol, and high-quality flour, in a market projected to exceed $312 billion by 2035; and (3) a structural shift in global supply chains as China diversifies away from Thailand and Vietnam for cassava inputs. Together, these forces create a rare, time-sensitive window for investors, processors, and policymakers willing to act with conviction.

The deeper structural opportunity lies in translating these productivity gains into participation in global fresh cassava markets, currently dominated by Colombia and Costa Rica not because their cassava is superior, but because their cold chain logistics and regulatory compliance frameworks are more mature. Fresh cassava export is technically demanding, post-harvest physiological deterioration begins within 24–72 hours and demands a tightly sequenced architecture of food-grade waxing within two to four hours of harvest, continuous 12–15°C cold chain, modified atmosphere packaging, EU phytosanitary and EUDR compliance, and TRACES NT pre-notification. Significantly, the digital tools already deployed along the corridor traceability platforms, integrated farm management systems, and trade connectors constitute the same audit-ready infrastructure that EU export demands. The remaining bottleneck is therefore not technological but logistical; the farm-to-port cold chain linking production zones to Tema, Lagos, and Abidjan. Closing that single gap would unlock a first-mover opportunity, anchored in geographic proximity to Europe, established diaspora demand, and the corridor’s existing institutional foundation in agricultural

traceability and would reposition cassava industrialisation as not merely a domestic ambition but a global export proposition.

“Africa grows 64% of the world’s cassava yet captures less than 1% of global export value. The Lagos–Abidjan corridor alone has the raw material base to reset this equation if capital, policy, and processing infrastructure align now.”

The Lagos–Abidjan corridor: West Africa’s economic spine

The Lagos–Abidjan Corridor is not merely a road. It is the circulatory system of West Africa’s most dynamic economic zone, a coastal strip connecting Nigeria’s commercial capital to Côte d’Ivoire’s port city through three smaller but strategically pivotal countries; Benin, Togo, and Ghana. This single corridor processes over 75% of ECOWAS trade by volume, with the transport sector alone contributing 5–8% of the region’s GDP.

Construction on the 1,028-kilometre six-lane dual-carriage Abidjan–Lagos Highway is scheduled to begin in 2026 and reach completion by 2030, backed by $15.5 billion in committed investment interest from the African Development Bank, bilateral partners, and private sector players. Dedicated freight lanes, intelligent transportation systems, and upgraded border-crossing facilities are integral to the design. For cassava, a highly perishable, bulky commodity with steep post-harvest losses, this infrastructure is transformative. Lower logistics costs, reduced transit times, and formalised cross-border trade will directly improve the economics of processing and export across the corridor.

Production: Raw materials advantage hiding in plain sight

Nigeria is, by a staggering margin, the world’s largest cassava producer. In 2023, the country harvested approximately 62–63 million tonnes, nearly 20% of total global output from over 10 million hectares concentrated in the humid south and guinea savanna zones. This single country produces more cassava than Thailand and Vietnam combined, yet its global export share remains negligible. Nigeria’s cassava is feeding over 200 million people domestically through staples such as garri (eba), fufu, and cassava flour; a food security anchor of incalculable value but the industrial and export potential is barely scratched. Ghana is the corridor’s second engine. Output grew from 8.1 million tonnes in 2000 to over 22.45 million tonnes by 2019, with a per-hectare yield of 23 tonnes in 2020 among the highest in Africa, reflecting the impact of improved varieties and agronomic investment. Côte d’Ivoire, Benin, and Togo contribute smaller but growing volumes, with significant area expansions recorded in all three countries over the past decade. Altogether, the five corridor countries produce a surplus of raw cassava that no processing sector, domestic or regional has yet come close to absorbing.

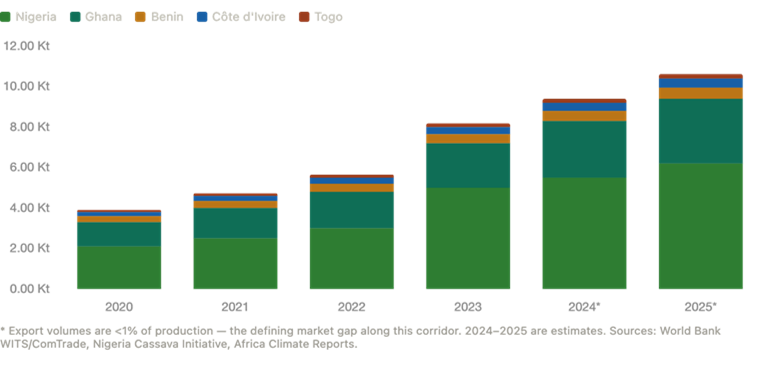

“Nigeria exports barely 5,000 metric tonnes of cassava products annually, less than 0.01% of its production while simultaneously importing processed cassava derivatives it has every capacity to manufacture domestically. This is not a resource problem. It is an infrastructure and investment problem.”

Post-harvest losses compound the challenge. Without adequate cold chain infrastructure, processing facilities, and organised collection systems, an estimated 20–40% of harvested cassava roots rot within 48–72 hours. Every tonne lost to spoilage is a tonne that could have generated $264–$450 in starch, or multiples more in downstream derivatives. Reducing post-harvest losses by just 10% at corridor scale would release millions of additional tonnes for value addition annually.

Consumption: A deep, growing domestic market

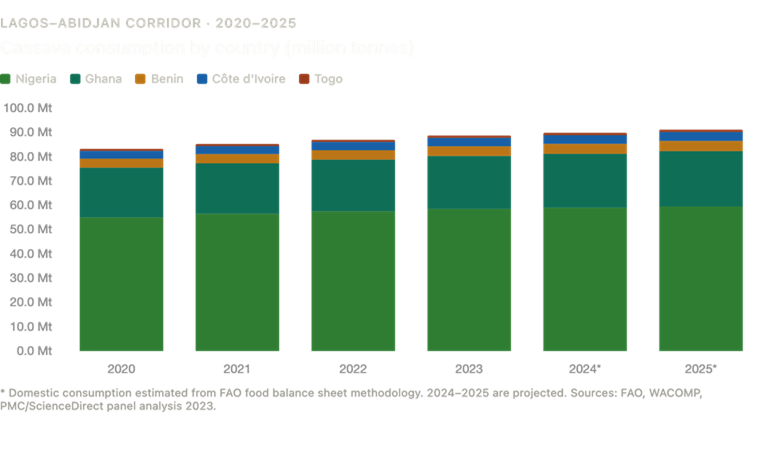

Cassava is not merely a crop along this corridor; it is a culture, sustenance, and daily economic activity rolled into one. Sub-Saharan Africa records the world’s highest per capita cassava consumption, approximately 800 grams per person per day. Ghana registered the highest per capita figure in 2019 at 646 kilograms per person per year. Nigeria’s southern populations depend on cassava as their primary caloric source. Garri, the roasted cassava granule, is a foremost staple across Nigeria, Ghana, Benin, and Togo alike; a staple food, a street snack, and an informal trade currency all at once. Africa’s total cassava consumption more than doubled between the early 1960s and the late 1990s, and the trajectory has continued upward. Urbanisation is reshaping consumption patterns in ways that create new commercial opportunities. Urban consumers prefer the convenience of shelf-stable processed forms; HQCF for baking products (bread, cake etc), packaged garri, fortified blends, over raw roots. This shift from subsistence consumption to market consumption is precisely the dynamic that industrial processors need to capitalise on. The market is not evolving, it is already here, growing rapidly, and presently served by imports that should be produced domestically.

Processing and value addition are the missing middle

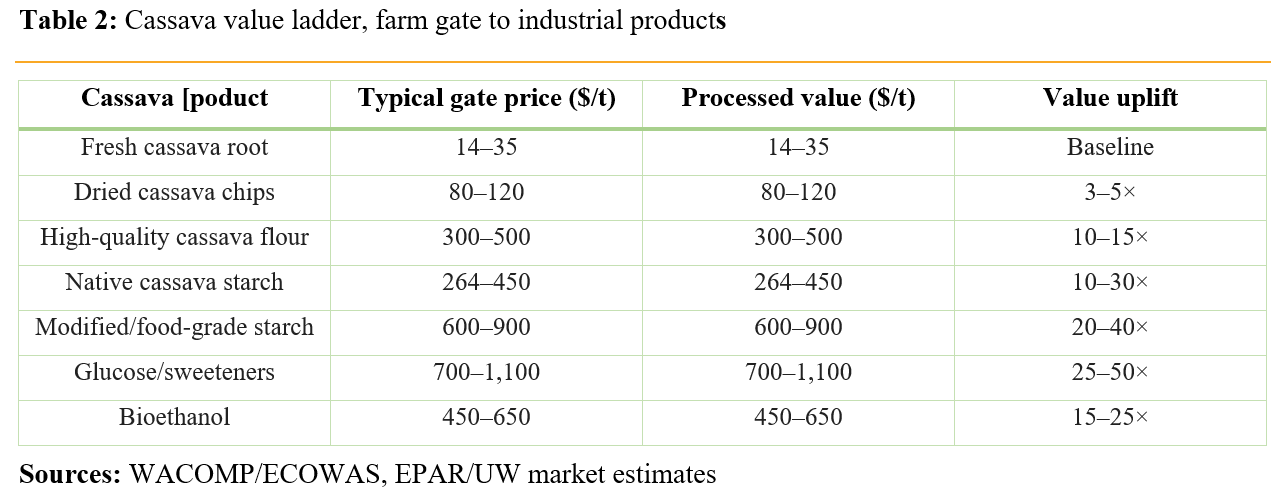

If production is the corridor’s sleeping giant, processing is its critical missing middle. The value destruction currently happening between farm gate and final use is staggering. Fresh cassava roots fetch $14–35 per tonne at source. The same cassava, converted to native starch, commands $264–450 per tonne, a 10–30-fold value uplift. Transformed into glucose or sorbitol, the premium is wider still. As high-quality cassava flour (HQCF) certified for industrial baking substitution, it enters a global food ingredients market worth billions annually. As bioethanol, it plugs into a $162 billion global biofuels market projected by 2032.

The processing landscape along the corridor is beginning to shift. In Nigeria, Dufil Prima Foods commissioned a 200-tonne-per-day HQCF plant in 2024 representing approximately ₦13 billion in investment. Flour Mills of Nigeria (FMN) has committed approximately $100 million to industrial starch processing. Olam Group launched a new cassava starch processing unit in Nigeria in March 2024. These are meaningful signals but against a backdrop of 62 million tonnes of annual production, the installed processing capacity remains a rounding error.

Ghana offers a complementary processing environment to Nigeria’s scale advantage. With high yields and active ECOWAS West Africa Competitiveness Programme (WACOMP) support, Ghana has developed a functioning HQCF cottage industry and is investing in international-standard starch and flour processing. The country’s relative political stability, port infrastructure at Tema, and linkages to European and Asian buyers make it an ideal location for export-oriented cassava industrialisation within the corridor.

Trade and export are the glaring untapped frontiers

The data on cassava trade from this corridor is, frankly, embarrassing given the resource base. ECOWAS; a bloc that produces over a third of the world’s cassava accounts for less than 1% of global cassava export value. Nigeria, the world’s single largest producer, exported approximately 5,000 metric tonnes of cassava products in 2023, less than 0.01% of its own production. Its top three export destinations were the United States, Ghana, and Namibia, collectively accounting for 81% of a minuscule total. Nigeria exported cassava

starch to Ghana in 2023 to the value of just $380,000, a bilateral trade figure that should be hundreds of millions of dollars annually.

Meanwhile, on the other side of the globe, China imported 2.05 million tonnes of cassava starch between January and July 2024 alone, valued at $1.08 billion, almost entirely from Thailand and Vietnam. China imports approximately 5 million metric tonnes of cassava chips annually, valued at over $1 billion, primarily to feed its vast ethanol production sector. The global cassava starch market is forecast to sustain strong growth through 2035 as demand for biodegradable plastics, pharmaceutical excipients, paper, textiles, and food-grade sweeteners accelerates worldwide.

“China is actively diversifying its cassava supply chain away from Thailand and Vietnam, constructing processing facilities in Laos, reducing dependence on legacy suppliers. West Africa is the natural alternative source. But to seize this window, the corridor must invest in drying, pelletising, and grading infrastructure now, not in five years.”

Regional intra-ECOWAS trade in cassava products such as garri, fufu, fresh roots, and chips is conducted overwhelmingly informally, dominated by smallholder farmers and small-scale cross-border traders. While this informal trade plays an irreplaceable food security role, it generates no traceable value, no tax revenue, no quality premium, and no platform for institutional investment. Formalising and scaling this trade through graded commodity exchanges, warehouse receipt systems, and regional quality standards is one of the highest return-on-investment interventions available to corridor policymakers today.

Investable opportunities: Where to place your capital

The Lagos–Abidjan corridor presents a structured spectrum of investment opportunities across the cassava value chain from primary production to processing, logistics, finance, and market development. Below, I outline the seven most compelling opportunity clusters for investors operating at different risk-return thresholds.

Industrial cassava starch processing facilities: The corridor produces tens of millions of surplus tonnes of cassava annually yet imports food-grade and industrial starch at premium prices. A modern starch processing plant of 100–500 tonnes per day throughput, deployable in Nigeria (Ogun, Oyo, Cross River), Ghana (Brong, Ahafo, Eastern Region), or Benin can convert raw cassava at $20/tonne into starch worth $400–$900/tonne. With China now offering zero tariff on imports from Africa and actively seeking new starch suppliers beyond Southeast Asia, export off-take agreements are achievable. Target internal rate of return between 22 and 30%. Capital requirement estimated at $5M–$50M per facility. Enabling policy ask for feedstock aggregation support and duty-free equipment import.

- High-quality cassava flour (HQCF) substitution industry: Nigeria and Ghana each import wheat flour worth hundreds of millions of dollars annually, flour that can be partially or fully substituted with HQCF certified to international standards (SON/GSA/CODEX). Government mandates in Nigeria (10% cassava flour inclusion in bread flour) provide guaranteed demand signals. The HQCF market has been validated by Dufil’s 200 t/day plant (2024). Opportunity here is the mid-scale HQCF plants ($2M–$10M) co-located near production clusters, linked to artisan bakers, fast food chains, and institutional buyers (prisons, military, schools). Investible format ideally through an SPV with offtake contracts.

- Cassava-based bioethanol and bioenergy plants: The global ethanol market stood at $99 billion in 2022, projected to reach $162 billion within the decade. West Africa has no meaningful cassava-to-ethanol capacity despite commanding the world’s largest cassava surplus. Cassava’s high starch content (25–30%) makes it technically superior to many competing feedstocks for bioethanol conversion. Blended fuel mandates and aviation biofuel targets across the corridor countries create policy momentum. Opportunity lies in greenfield 10–50 million litre/year bioethanol plants in Nigeria or Ghana, ideally co-located with starch processing for maximum cassava utilisation and waste valorisation.

- Cassava chips export infrastructure (China & Asian markets): China imports 5 million tonnes of cassava chips annually, valued at over $1 billion. African cassava chips if properly dried, graded, and containerised, can compete on quality and cost with Thai and Vietnamese chips, especially as geopolitics and China’s diversification push create structural demand for African alternatives. The immediate infrastructure need is drying and pelletising capacity at farm cluster level, linked to container-stuffing facilities at Apapa (Lagos), Tema (Accra), Lomé, Cotonou, and Abidjan ports. Capital requirement estimated between $500K–$3M per drying/pelletising hub. ROI can be de-risked through export off-take agreements with Chinese trading companies.

- Cassava-based sweeteners, glucose, fructose & sorbitol: Regional demand for cassava-based sweeteners (glucose, fructose, sorbitol) across African markets excluding Nigeria already stands at 300,000–400,000 metric tonnes annually. This demand is currently met by imports; a foreign exchange drain that is entirely avoidable. The manufacturing process for glucose syrup from cassava starch is well-established; the investment case requires integrated starch + saccharification + refining capacity. First-mover advantage in this sub-segment is significant. The beverage, confectionery, pharmaceutical, and personal care industries across the corridor represent a captive, import-substitution market worth $200M–$400M per year at current import parity prices.

- Cold chain, logistics & aggregation infrastructure: Post-harvest losses of 20–40% represent the single largest value destroyer in the corridor’s cassava economy. Solving this problem is simultaneously a humanitarian intervention and a commercial opportunity. Mobile cassava processing units (MPUs), solar-powered drying infrastructure, climate-controlled aggregation centres, and digital farm-to-processor linkage platforms represent a $200M+ investment gap across the five corridor countries. The $538M Special Agro-Processing Zones (SAPZ) Programme backed by AfDB, IFAD, and IsDB provides concessional capital that can be blended with private equity to de-risk first-mover logistics investments. The Abidjan–Lagos Highway, once operational (2030), will significantly improve the unit economics of corridor-wide cold chain networks.

- Cassava animal feed integration: Cassava peels, pulp, and by-products from processing are high-energy feed resources currently wasted at scale. In Nigeria, cassava already accounts for 54.7% of the sub-region’s use as livestock feed (FAO, 2009), almost entirely from unorganised, informal use. A formalised cassava-based animal feed industry combining dried peels, cassava pulp with protein supplements, and fortification minerals can absorb processing waste streams and generate a high-margin by-product revenue line. With West Africa’s poultry, aquaculture, and swine sectors growing at 6–8% annually, demand for affordable, locally produced feed ingredients is structurally robust. Target markets: Nigeria (poultry), Ghana (fish feed), Côte d’Ivoire (cattle).

Policy imperatives: What governments must do now

Private capital follows certainty. The cassava value chain along the Lagos–Abidjan corridor will not unlock at the scale its resource base justifies without deliberate and coordinated policy action. Five imperatives stand above all others.

First, our corridor governments should enforce and expand cassava flour inclusion mandates. Nigeria’s 10% HQCF inclusion policy for wheat flour is a powerful demand stimulus but enforcement has been inconsistent. Ghana and Côte d’Ivoire should adopt analogous policies. A unified ECOWAS-level HQCF standard and inclusion mandate would create the scale of demand that justifies industrial investment.

Second, we should fast-track the Agro-Processing Zones. The $538M SAPZ Programme must be disbursed efficiently and the zones operationalised with investor-ready infrastructure including power, water, roads, and logistics before competing jurisdictions attract the processing capital this corridor needs. Nigeria’s six SAPZ sites and Ghana’s equivalent zones should prioritise cassava-anchored tenants (agro-parks).

Third, we establish a corridor-wide cassava commodity exchange. Formalising intra-ECOWAS cassava trade through graded commodity standards, warehouse receipt systems, and price discovery mechanisms would attract financial institutions and commodity traders, reduce informal trade friction at borders, and create the price transparency that investors require to underwrite processing investments.

Fourth, we must harmonise phytosanitary and quality standards. Cassava chips, starch, and flour face different certification requirements in each corridor country and at export destinations. A harmonised ECOWAS Cassava Product Quality Standard aligned with Codex Alimentarius, would eliminate a major non-tariff barrier to intra-regional and intercontinental trade.

Fifth, we must create investment-grade cassava data. Investors cannot act on imprecise data. The corridor urgently needs a real-time, open-access cassava production and price database disaggregated by country, variety, region, and product form, comparable to the data infrastructure that supports commodity investment in Southeast Asia.

The window will not stay open forever

The cassava opportunity along the Lagos–Abidjan corridor is not a hypothesis. It is a documented, data-verified market gap sitting at the intersection of abundant raw material, surging global demand, and transformative infrastructure investment. The corridor grows more cassava than the entire country of Thailand, the world’s dominant cassava exporter yet Thailand’s cassava export earnings dwarf Africa’s by orders of magnitude. That gap is capital, that gap is processing, and that gap is policy coherence.

The highway breaking ground in 2026 is a once-in-a-generation infrastructure event. China’s active search for alternative cassava supply chains is a once-in-a-decade trade opportunity. The SAPZ Programme’s $538 million in concessional finance is a once-in-an-era public investment catalyst. These windows are open simultaneously right now. Investors who move in the next 24–36 months will establish positions that will compound for decades. Those who wait for the corridor to be fully developed will pay the price of late entry.

The Lagos–Abidjan corridor cassava sector is the most compelling agricultural investment thesis in sub-Saharan Africa today. The raw material base is unmatched. The markets, domestic, regional, and global are hungry and growing. The infrastructure is arriving. What the sector needs now is you: investors with patience, processors with technology, policymakers with discipline, and stakeholders with the courage to act on data rather than wait for consensus.

Africa produces the world’s cassava. It is past time Africa captured the world’s cassava value.

Source: Dr. Kojo Ahiakpa